Insurance Acceptance Explained for Healthcare Patients

TL;DR:

- Accepting your insurance means a provider is in-network but does not guarantee full coverage for all treatments.

- Prior authorization, claim denials, and complex rules influence whether costs are ultimately covered, requiring patient vigilance.

When your doctor’s office says they “accept your insurance,” most patients assume that means their care is covered. That assumption is where confusion and unexpected bills are born. Insurance acceptance explained properly means understanding that a provider agreeing to work with your insurer is just the starting point. What follows, from prior authorization requirements to claim denials and patient protections, is a process with its own rules, timelines, and rights. This guide walks you through exactly how insurance acceptance works and what you can do to protect yourself.

Table of Contents

- Key takeaways

- Insurance acceptance explained: what it really means

- Prior authorization: why it slows things down

- Understanding claim denials and your right to appeal

- Patient protections you may not know about

- Applying this knowledge to your own healthcare

- My perspective on insurance acceptance realities

- How Gardenstatemedicalgroup supports your insurance journey

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Acceptance is not full coverage | A provider accepting your insurance means they are in-network, not that all treatments are automatically covered. |

| Prior authorization adds a step | Many treatments require insurer approval before care is delivered, and delays are common. |

| Denials can be appealed | Fewer than 1% of patients appeal denied claims, but appeals succeed more often than most people realize. |

| Federal laws protect you | The No Surprises Act shields you from unexpected bills during insurer-provider payment disputes. |

| Verification saves money | Confirming coverage details before your appointment prevents costly surprises after care is received. |

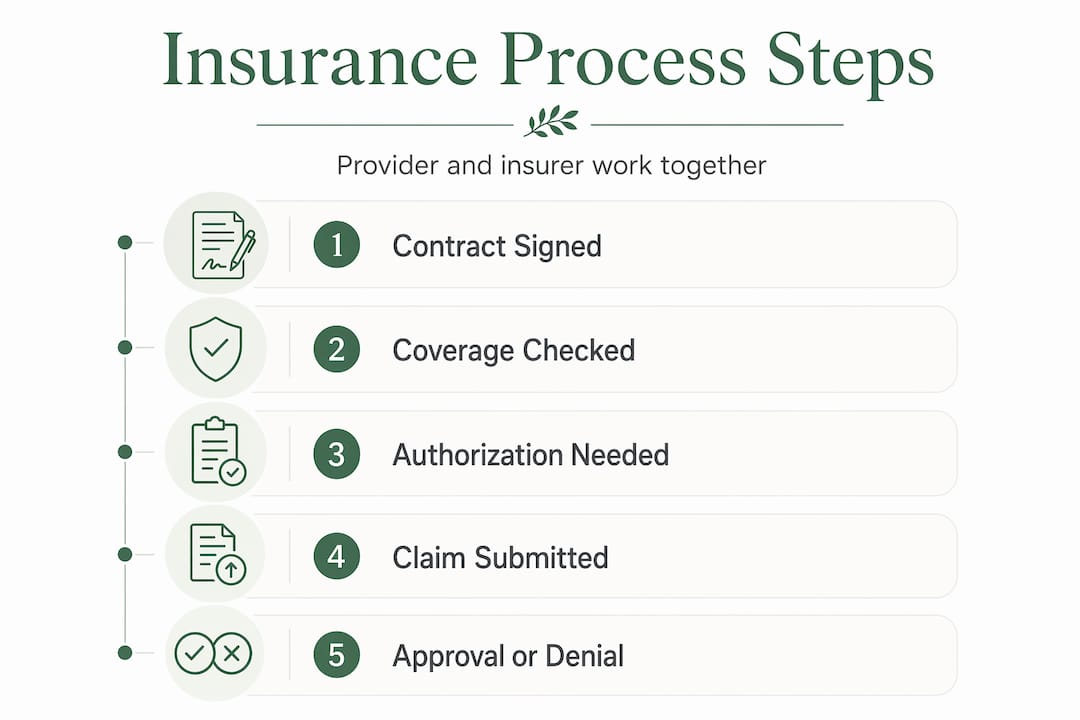

Insurance acceptance explained: what it really means

Understanding insurance acceptance starts with one key distinction. When a provider accepts your insurance, they have signed a contract with your insurer agreeing to participate in that insurer’s network. That agreement sets negotiated rates for services and establishes billing rules. It does not mean every service you receive will be paid for automatically.

Think of it this way. The insurance policy approval process involves two separate agreements working together. The first is between you and your insurer, which establishes your eligibility and covered benefits. The second is between your insurer and your provider, which determines billing rates and network status. Both need to align for a claim to be paid.

Insurance eligibility criteria matter here. Your plan has a defined list of covered services, and your insurer uses written clinical guidelines to determine what qualifies for coverage. Medical necessity is one of those criteria. A service is considered medically necessary when it meets the insurer’s specific clinical standards, not simply because your doctor recommends it.

Pro Tip: Before scheduling any non-routine care, ask both your provider’s office and your insurance company whether the specific procedure code is covered under your plan. Getting that confirmation in writing gives you a reference point if a dispute arises later.

It also helps to know that insurance acceptance works differently for primary care versus specialist visits, imaging, labs, and procedures. Each category can carry its own rules about referrals, prior authorization, and cost-sharing amounts.

Prior authorization: why it slows things down

Prior authorization is the process where your insurer reviews and approves a treatment, medication, or procedure before it is delivered. It exists so insurers can confirm that the requested service meets their coverage criteria. For patients managing chronic conditions or scheduled for specialist care, prior authorization is a frequent hurdle.

The administrative weight of prior authorization falls heavily on both patients and providers. Delays in approval can push back surgery dates, interrupt medication access, and add stress to already difficult health situations. Only 1 in 3 physicians trusts insurers’ promises to reduce prior authorization burdens, which tells you something about the gap between stated policies and day-to-day practice.

The federal government has stepped in with meaningful reforms. CMS now requires impacted payers to issue prior authorization decisions within 72 hours for urgent requests and within 7 calendar days for standard requests. This change is projected to save approximately $15 billion over 10 years by reducing administrative costs. Electronic prior authorization, which replaces phone calls and fax submissions with direct digital exchanges between provider and insurer systems, is part of this modernization effort.

Here is how you can navigate prior authorization as a patient:

- Ask your provider’s office whether prior authorization is required before your appointment or procedure.

- Confirm that the authorization request has been submitted and get a reference number.

- Follow up with your insurer directly to verify that approval was received before your scheduled date.

- If authorization is denied, ask your provider to request a peer-to-peer review immediately.

- Document all communications, including dates, names, and reference numbers.

“A peer-to-peer review, where your physician speaks directly with the insurer’s medical director, is often the fastest way to overturn a prior authorization denial. Request it within 5-10 business days of denial for maximum effectiveness.”

Pro Tip: Keep a dedicated folder, physical or digital, for all prior authorization correspondence. If a denial goes to appeal, having a complete paper trail speeds up the process considerably.

Understanding claim denials and your right to appeal

A claim denial does not mean the conversation is over. It means your insurer has reviewed the claim and determined, based on their criteria, that they will not pay it at this time. The reasons vary, and knowing the specific reason behind your denial is the most important first step.

Common reasons for claim denials include:

- Medical necessity: The insurer determined the service did not meet their written clinical guidelines. Insufficient documentation is the most frequent trigger, not clinical disagreement.

- Prior authorization missing: The service was delivered without required advance approval.

- Out-of-network provider: You received care from a provider outside your plan’s network.

- Billing errors: Incorrect procedure codes or missing patient information on the claim form.

- Duplicate claim: The same service was billed more than once.

Here is a sobering reality about appeals. Fewer than 1% of denied claims were appealed by patients in 2024, yet insurers upheld 66% of those appeals. That means when patients do push back, they succeed in reversing the denial nearly two-thirds of the time. Most people simply do not know they can appeal or assume it will not work.

| Step | What to do |

|---|---|

| Read the denial letter carefully | Identify the exact reason code and clinical criteria cited by the insurer. |

| Request full criteria documentation | The denial letter must include the clinical criteria; request this at no cost if it is missing. |

| File an internal appeal | Submit a formal appeal with your physician’s supporting notes and medical records. |

| Request a peer-to-peer review | Have your doctor contact the insurer’s medical director to discuss the clinical case directly. |

| File an external appeal | If the internal appeal fails, escalate to an independent external reviewer as allowed under the ACA. |

Under the ACA’s appeals framework, you have the right to both an internal appeal and an independent external review for denied marketplace plan claims. Patients can also cite ACA §2719 to reinforce their rights during this process. If your plan is through the marketplace and your insurer fails to respond appropriately, filing a complaint with CMS is a valid next step.

Pro Tip: Do not accept vague denial language. Your insurer is required to tell you which specific clinical criteria your claim did not meet. If the denial letter is unclear, call and ask for it in writing before drafting your appeal.

Patient protections you may not know about

Federal law has built meaningful protections into how insurance acceptance works for patients, particularly around surprise billing. These protections matter most when you have done everything right and still end up in a billing dispute.

The No Surprises Act, which took effect in 2022, is the most significant recent change. Here is what it covers:

- Emergency care: You cannot be billed at out-of-network rates for emergency services, regardless of which hospital or facility treated you.

- Non-emergency care at in-network facilities: If you receive care at an in-network hospital or facility and an out-of-network provider is involved without your advance knowledge or consent, balance billing is prohibited.

- Your cost-sharing: You pay only the in-network cost-sharing amount. The financial dispute between the insurer and the out-of-network provider is resolved through independent arbitration, without involving you.

- Good Faith Estimates: Providers must give uninsured or self-pay patients a written cost estimate before scheduled services. If your bill exceeds that estimate by $400 or more, you have the right to dispute it.

These protections do not solve every insurance challenge, but they do remove patients from the middle of insurer-provider payment disputes. That is a meaningful shift from how billing worked just a few years ago.

Applying this knowledge to your own healthcare

Understanding how insurance acceptance works gives you real tools to manage your care and avoid unexpected costs. This is especially true if you are managing a chronic condition that requires ongoing specialist visits, prescription medications, or regular diagnostic testing.

- Verify coverage before every appointment. Call your insurance company and confirm that your specific provider and the specific services you need are covered under your current plan. Checking coverage details takes 10 minutes and can prevent bills totaling thousands of dollars.

- Know your plan’s prior authorization requirements. Ask your primary care physician which referrals and procedures typically require advance approval. This is especially relevant for imaging, specialist consultations, and surgical procedures.

- Keep records of every interaction. Write down the date, the name of the representative you spoke with, and what was confirmed during every call with your insurer or provider’s billing department.

- Act quickly after a denial. Most plans have strict timelines for filing appeals, often 30 to 180 days from the denial date. Missing the deadline forfeits your right to appeal.

- Use available resources. Your provider’s billing team, your state insurance commissioner’s office, and patient advocate organizations can all help you navigate disputes when they get complicated.

Knowing your rights under the No Surprises Act and the ACA puts you in a much stronger position when something does not go as expected. The impact of provider choices on coverage and care access is real, and being informed allows you to make choices that protect both your health and your finances.

Pro Tip: If you are managing a chronic condition, ask your primary care provider to document your ongoing treatment plan thoroughly. Detailed clinical notes reduce the likelihood of medical necessity denials and strengthen any appeal you may need to file.

My perspective on insurance acceptance realities

I have spent years watching patients navigate the gap between what their insurance card promises and what actually gets paid. The frustration is real and it is valid.

What I have come to believe is that most patients lose coverage battles they could have won because they did not know the rules. A denial feels final. It is not. The appeals process is underused, and when patients take the time to understand the clinical criteria their insurer cited and respond with proper documentation, reversals happen more often than not.

I have also seen how new laws like the No Surprises Act genuinely protect patients who previously had no recourse. Progress is real. But the system still requires patients to be active participants, not passive recipients.

My honest advice: treat your insurance like a contract you need to understand, not just a card you hand over at the front desk. Ask questions before care, not after. Document everything. And when something goes wrong, push back.

— Krunal

How Gardenstatemedicalgroup supports your insurance journey

At Gardenstatemedicalgroup, understanding your insurance coverage should never be something you face alone. The practice accepts a wide range of insurance plans, and you can review the full list of accepted insurance plans to confirm your coverage before your first visit. Whether you are starting with primary care services or managing a long-term condition through the chronic care management program, the team at Gardenstatemedicalgroup is experienced in working with your insurer to support coordinated, continuous care. Patients in North Bergen and Secaucus can contact the practice directly to get personalized guidance on coverage, referrals, and prior authorization support before care begins.

FAQ

What does insurance acceptance mean for patients?

Insurance acceptance means your healthcare provider has a contract with your insurer and participates in their network. It means you pay negotiated in-network rates, but it does not guarantee that every treatment or service you receive will be covered.

Why do insurance claims get denied even when my provider accepts my insurance?

Claims are denied for reasons such as missing prior authorization, failure to meet medical necessity criteria, or billing errors. Most denials have nothing to do with the insurer-provider agreement and can be appealed successfully with the right documentation.

How long do I have to appeal a denied insurance claim?

Most health plans allow between 30 and 180 days from the denial date to file an internal appeal. Under ACA rules, you also have the right to request an independent external review if your internal appeal is unsuccessful.

What is the No Surprises Act and how does it protect me?

The No Surprises Act prevents providers and insurers from billing you at out-of-network rates for emergency care or for services at in-network facilities when you did not choose an out-of-network provider. You pay only your standard in-network cost-sharing amount.

How do I find out if a specific service requires prior authorization?

Call your insurance company directly and provide the procedure code your provider plans to bill. Your provider’s office can also check on your behalf, which is the most efficient option when the procedure is being ordered.